Student Loans: Recent Policy Actions and the Path Forward

Field Note #1

Recent federal changes to student loan policy are changing the way students finance their education.

Background

Section 8101 of Public Law No: 119-21, the One Big Beautiful Bill Act (OBBB) added new loan limits for graduate students, professional students, and parents borrowing on their behalf. Additionally, Graduate PLUS loans were eliminated for future borrowers, and the groups able to identify as professional students were redefined.

After the passage of OBBB, the Department of Education (ED) published a proposed rule on January 30, 2026, titled “Reimagining and Improving Student Education”. A press release was issued by ED announcing the proposed rule and partly stated, “…These new caps will compel colleges and universities to prioritize students, and incentivize institutions to reduce tuition and fees, making higher education more affordable and preventing students from being burdened with unmanageable debt after graduation.”

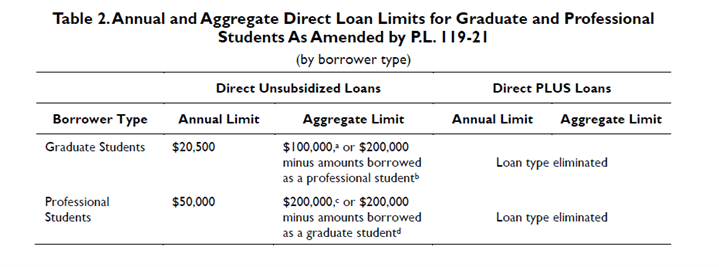

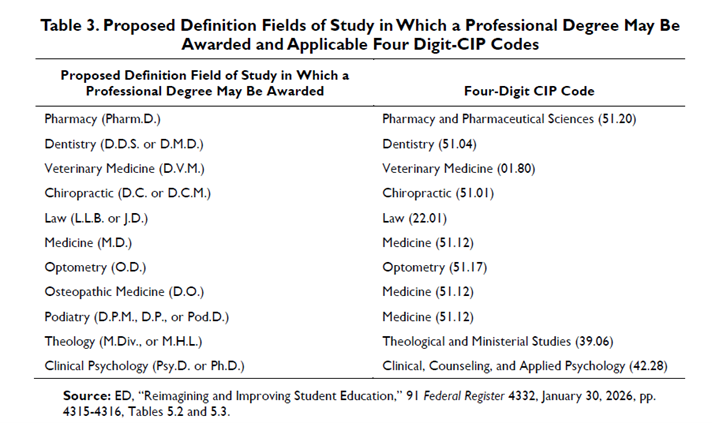

The Congressional Research Service (CRS) published an analysis of the proposed rule, including summaries of key changes on federal student loan borrowing limits beginning in July 2026. Page 4 of the CRS report displays a table describing the new loan limits while page 8 shows the fields of study described as professional degrees under new guidelines. Both tables are included below:

Congressional Budget Office estimates for the new law show savings from the implementation of Section 8101 are expected to be approximately $44.17 billion, from the years 2025 to 2034.

A New Landscape

A more limited supply of federal loans means more private companies will be ready to grab potential clients. An article from last September in Forbes detailed how well-known lenders can benefit from the new regulations and stated, “…Market leader Sallie Mae told investors that the federal loan limits could eventually add $4.5 to $5 billion annually to its loan originations, which totaled $7 billion in 2024. Other publicly traded companies in line to benefit include SoFi and Navient…”

The White House issued a press release on November 24, 2025 addressing issues raised on the education front about professional degrees. When addressing what was described as the myth of tuition rising due to the changes, the release stated “…Since 2007, graduate and professional students have been able to borrow up to the full cost of attendance. This has allowed colleges and universities to dramatically increase tuition rates, even for credentials with modest earnings potential, which has saddled too many borrowers with debts they find difficult to repay…” The last sentence of the release links to an article from the American Enterprise Institute which describes law schools modifying their tuition due to new federal regulations.

Concerns

One of the main concerns regarding the policy changes is that new loan limits will not be sufficient to cover tuition expenses. This is a concern shared by both graduate students and professional students. Professional students able to borrow more still hit limitations in affordability. Marci Lesh, a staff reporter for the Rocky Mountain Collegian, wrote specifically about veterinary students (defined as professional students in new regulations) and costs still causing worry. A student interviewed in the article, Zoe Dailey, was accepted into the Kansas State University (KSU) veterinary program and shared her concern for future applicants, partly stating, “…No one wants to be in financial distress,” Dailey said. “If they don’t have a way of getting that money, definitely students would be discouraged to apply.”

Future funding is a valid concern, especially for out-of-state students. The annual cost of studying veterinary medicine at KSU as a non-Kansas resident is approximately $60,476 for “estimated tuition and mandatory fees”, according to university’s Office of Student Financial Assistance. Adding other expenses (housing, e.g.) can bring the cost to approximately $81,102. The policy of limiting loan amounts leads to the concern of advanced degrees remaining out of reach for certain students.

Recommendation

A prudent way forward includes tackling the issue of why students choose to take out loans, which continue to build interest over time. There was an interesting contract study that sought to evaluate the effectiveness of providing borrowers with two additional years of loan counseling. Evaluations of Federal Financial Aid Information and Delivery Strategies: An Experiment Requiring Additional Loan Counseling for Student Borrowers was established in 2018 and the background statement partly states, “The Institute of Education Sciences was to have assessed the effectiveness of these waivers on students' borrowing and college progress and, later, loan repayment.”

Cancelled in February 2025, the study’s webpage states the National Center for Education Evaluation and Regional Assistance (NCEE) “is evaluating what publications, if any, may arise from this work”. It would help future policy decisions to see evaluation results from any information provided to NCEE from the 35 colleges that volunteered to take part in the study. Recent changes to student loans do not negate the fact that decisions made by students need to be enacted under the best possible circumstances, which include ensuring borrowers maintain knowledge of how current loans impact future decisions.